Source: IFSWF Database, 2021.

For the best part of a decade, sovereign wealth funds have been looking to raise their allocations to unlisted assets, including private equity.

In the financial services industry, it is often assumed that this increased allocation would come at the expense of their allocations to listed equity. However, this appears not to be the case. Rather, sovereign wealth funds are seeking to generate real durable value by backing less mature companies, rather than simply recycling existing wealth, and boosting returns by occasionally making contrarian bets in times of market dislocation.

For example, one of the trends highlighted in our 2020 Annual Review was how sovereign wealth funds had ramped up their investments in public markets. This phenomenon resulted from several domestically focused sovereign funds investing in locally-listed companies to support their local economies at the peak of the pandemic. Concurrently, Saudi Arabia’s Public Investment Fund made some opportunistic investments in international blue-chip companies during the market rout of early 2020. A year later, sovereign wealth funds’ direct investments in listed companies are still relatively high, representing 40% of the total, but lower in relative and absolute value than the previous year.

Nevertheless, according to the latest research from State Street and IFSWF, sovereign wealth funds continue to increase their private-market investments for three reasons. First, they have long-term strategic asset allocation targets for private markets and are still building their private markets portfolios. Second, unlisted assets often help diversify sovereign wealth funds’ portfolios due to idiosyncratic opportunities, various risk-return spectrums and asymmetric information. Third, some sovereign wealth funds are embracing illiquidity premiums by allocating to private markets as they have long-term investment horizons.

Source: IFSWF Database, 2021.

“We believe we can target further value-add in private market opportunities, which also provide inflation protection and defensive characteristics,” said the Future Fund in a position paper in September 2021. “While also adding value in public markets, for example through more closely managing the use and costs of illiquidity,” added the Australian sovereign fund.

In short, as sovereign wealth funds have become more familiar with, and more experienced in private equity, they seem to be drawing less distinction between listed and unlisted equity, as they look for robust sources of return. As a result, in a very busy investment year, there were both record levels of investments in initial public offerings (IPOs) as well as in private companies at earlier stages of capital raising.

According to the consulting firm Ernst & Young, 2021 was the most active year for initial public offerings (IPOs) in the past 20 years, with 2,388 deals raising a total of $453.3 billion, global IPO activity was up 64% and 67% by deal numbers and proceeds, respectively.1 Unsurprisingly, it was a record-breaking year for sovereign wealth funds’ participation in IPOs. They invested a total of $5.1 billion in 71 deals, up 45% by equity and 108% by deal numbers. Asia led the way with $3 billion invested in 47 IPOs, 74% of which were in India. Indian IPOs were dominated by e-commerce and internet companies tapping the public markets.

Indian tech companies benefited from regulators in China – a major source of IPOs in digital companies – tightened regulation on local technology companies listing abroad, and at the same time, some Indian startups took advantage of a local ban on Chinese apps last year following a border clash between the two countries. A symbol of India’s stock market frenzy was the IPO of food delivery startup Zomato, which was oversubscribed by almost 40 times and had a list of 186 anchor investors, including three sovereign funds: ADIA, Singapore’s GIC and Norway’s Government Pension Fund Global (GPFG).

Indian startups, therefore, had fewer competitors to fight over for a slice of their home market of 1.3 billion people. Against this backdrop, more of India's digital companies are tapping into the stock market. Other companies backed by sovereign funds included beauty startup Nykaa, One97 Communications, parent of digital payment provider Paytm, and online insurance marketplace, Policybazaar.

Source: IFSWF Database, 2021.

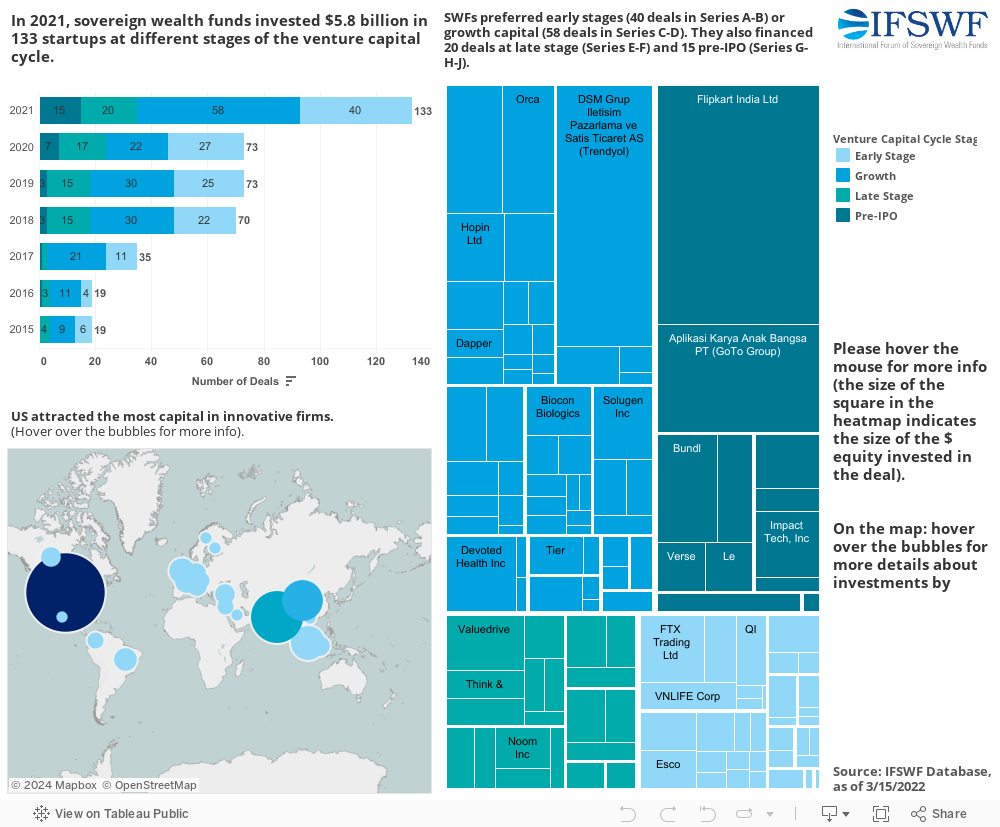

In 2021, sovereign wealth funds invested $5.8 billion in 133 startups at different stages of the venture capital cycle, almost 40% up from 2020 and 77% more transactions than the 75 that year. Sovereign wealth funds favoured investing at the growth capital stage (series C and D of equity raising), a total of $2.4 billion in 58 deals.

This confirms the findings of a survey of IFSWF members published in the report Partnering for success: Sovereign wealth fund investments in private markets in which 18 institutions out of 21 respondents said they allocated capital to growth-stage private equity.

Source: IFSWF Database, 2021.

Indian e-commerce startup Flipkart’s $3.6 billion series G, pre-IPO, equity raising was the largest round backed by four sovereign wealth funds: GIC, QIA, Malaysia’s Khazanah and Abu Dhabi’s strategic sovereign fund ADQ. The fundraising round valued the Indian online retailer at $37.6 billion, with the majority owner, Walmart, joining investors including SoftBank Group – which had exited when it sold a majority stake to Walmart in 2018 at a valuation of $22 billion.

2021, the second year of the COVID-19 pandemic, was a record year for sovereign wealth fund direct equity investments in both public and private markets as they sought to find pockets of higher risk-adjusted returns. Investments in public markets were driven by a buoyant M&A investment environment and by record levels of IPOs as many firms that stayed private the previous year, finally plucked up the courage to tap into the stock market. For larger start-ups, the so-called unicorns (early-stage, unlisted companies with valuations of at least $1 billion), the time from founding to IPO increased from seven years in 2015 to nearly 11 as of 2020.2

Sovereign wealth funds also committed record levels of investment in startups, particularly at the early stages and growth. “We believe we can target further value-add in private market opportunities, which also provide inflation protection and defensive characteristics,” wrote the Future Fund in September. “While also adding value in public markets, for example through more closely managing the use and costs of illiquidity,” added the Australian sovereign fund.

However, according to new research from State Street proprietary data and IFSWF members in April 2022, it appears that institutional investors, including sovereign wealth funds, started pulling out of some higher risk strategies in equity markets at the end of 2021 and beginning of 2022. This will only appear in next year’s annual review when we will be able to see how sovereign wealth funds have fronted the new challenges posed by a high inflation environment and further deglobalisation forces.

Copyright © 2021 IFSWF Ltd.